We previously discussed the similarities between incumbent insurers and incumbent banks in their approach to creating digital-only brands.

In Part 2 of the series, we will explore how a handful of Insurtechs have, similar to their fintech counterparts, developed innovative solutions that solve customer pain points. These pain points were previously deeply inherent in the insurance industry and include:

Tedious self-servicing, including claims management

A lack of tailored, personalised recommendations based on smart data putting the onus on the customer to shop around for better deals

Rigid, broad product offerings.

Tackling these pain points, we have seen a wave of innovators that have created new micro-services that ensure people are insured in a relevant, and personalised way and a digital overview of policies held with subsequent support in finding the best individual deal.

The first group of innovators in insurtech, those who have launched new micro-services, are primarily found in the automobile and comprehensive personal insurance spaces.

Essentially these firms have deconstructed the traditional, broad, inflexible insurance products. The second group has made it easier for consumers to manage multiple policies in one place, while simultaneously ensuring they are fully covered across the board and receiving the best possible price. Two leaders in this space come to mind.

Cuvva: Pay as you go insurance, with clever integrations

Cuvva is one of a kind in the world of customer experience and product offering. The UK based Insurtech offers a range of auto-insurances focused on shorter terms and spontaneous need, including both temporary car insurance and Learner driver insurance.

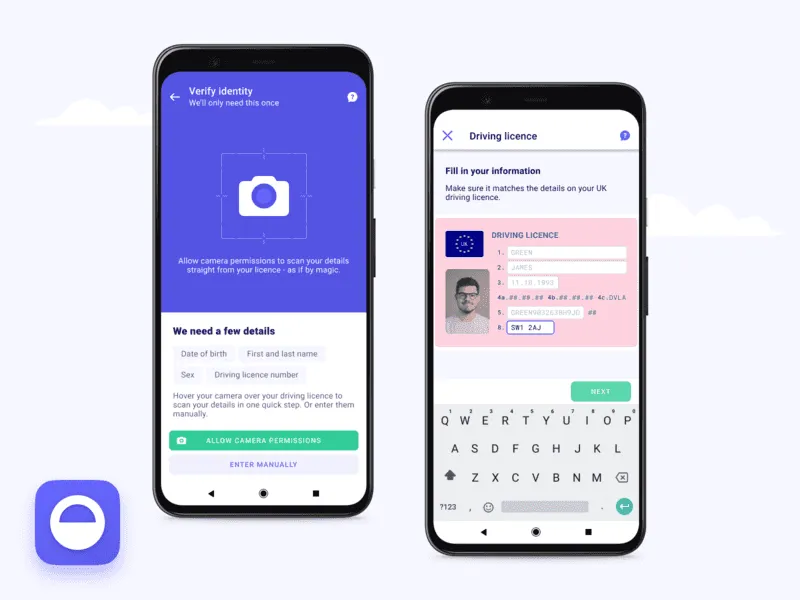

The application journey is completely relevant to its customer base. Given the fact that customers are likely to need temporary car insurance or Learner driver insurance on a bit of whim, the entire application journey can be completed in minutes, anywhere, and anytime. One of the great features of Cuvva is that it uses MyLicence, a solution offered by the UK Driver and Vehicle License agency.

The solution provides real-time driving licence data from the DVLA at point of quote, removing the need for secondary validation, a reduction in fraud, and a faster quotation and purchase journey. Cuvva makes more than 100,000 calls to MyLicence per month and use of the service is a requirement for 100% of new customer transactions.

Customers can scan their drivers license, which is confirmed with the DVLA in real-time

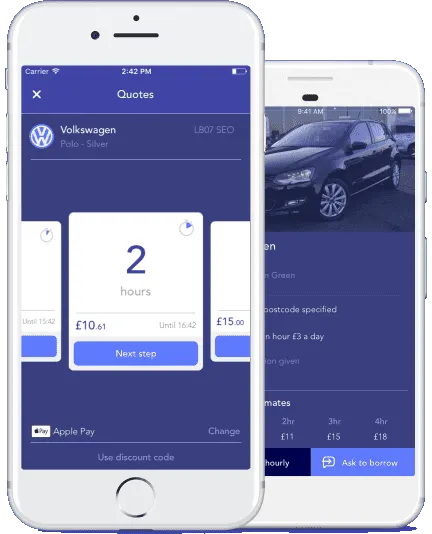

The product offerings from Cuvva are an example of a new, deconstructed micro-service. Cuvva was created to address the problem that nobody was offering short-term car insurance by the hour. With Cuvva, customers can be insured for as little as an hour, but Cuvva also offers Insurance in daily, weekly and monthly intervals. It covers use cases such as borrowing a car, taking a car for a test drive, or sharing a longer drive between a few people. During the application process, customers initially select the length of time they would like to be insured, but can easily extend the time in a few seconds. Pricing is transparent, and customers can pay via Apple Pay.

Ease of selecting the relevant product and ability to pay with Apple Pay

Clark: The epitome of relevance in a complex market

Similar to Cuvva in maintaining absolute relevance to its target customer segment, Germany-based Clark is perfect for the German market. Germans hold 6.5 policies on average and pay annual premiums of almost €2.5k, making it one of the top five largest insurance markets in the world.

The Clark platform is essentially two-fold: first it offers insurance advice, driven by robo-advisory and second, it utilises a team of certified insurance experts that are available to cover a range of insurance products. As of summer 2018, Clark had acquired over 100,000 customers. This translates into $310 million in contract volume.

Clark offers insurance advice via robo-advisory and a team of certified insurance experts that are available to cover a range of insurance products.

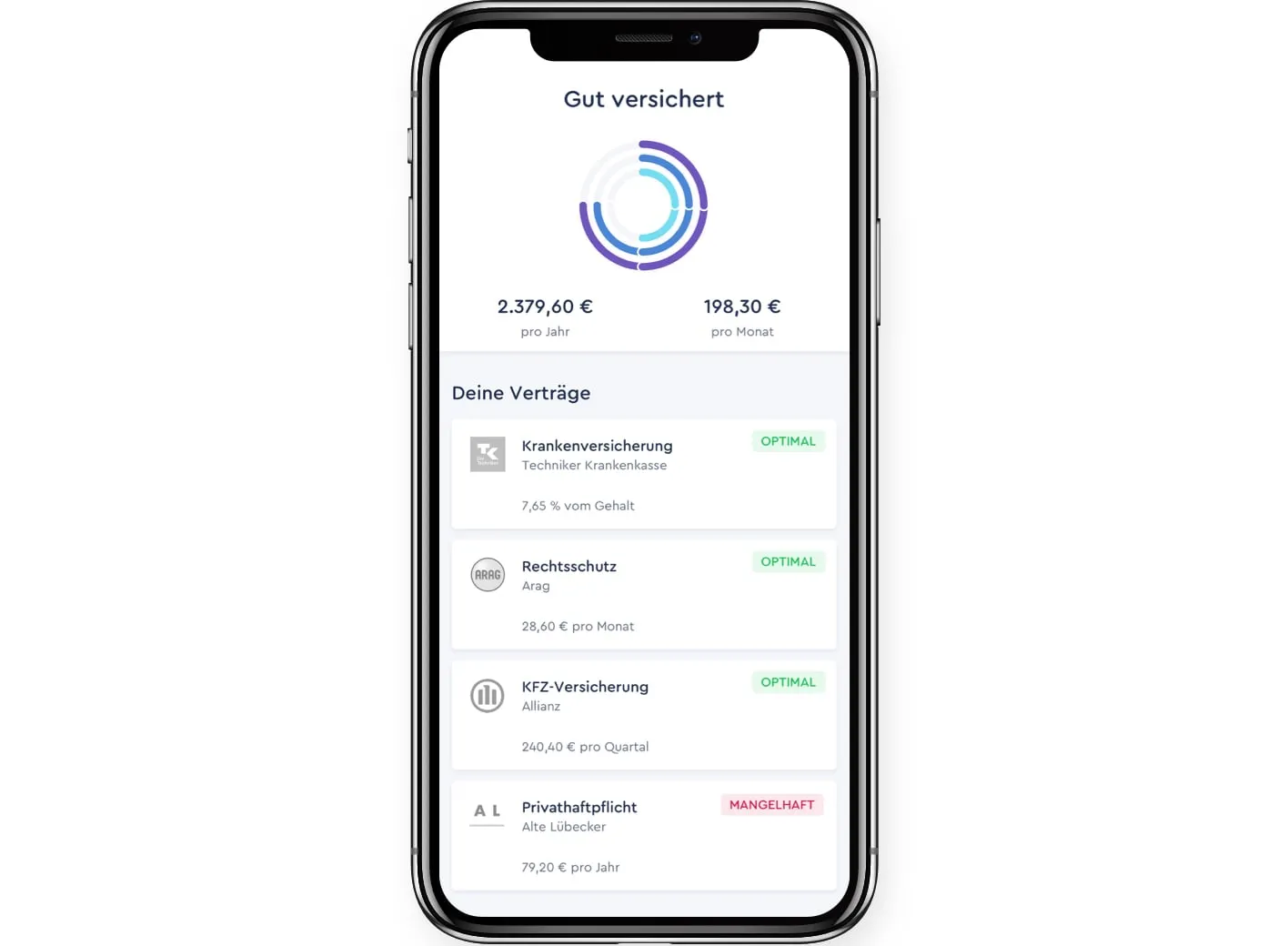

Clark is a one-stop shop for nearly everything related to managing insurances, namely by providing contract management, advice and fulfilment. The management feature provides a digital overview, which is in a sense a first for Germany. To understand how disruptive this digital view has been, it’s important to know that the Germany insurance industry is largely dominated by local “mom and pop” physical brokers (c. 50,000 brokers). This digital view provides customers with an overview of how much they are paying per year and month, provides access to notice periods and insurance numbers.

The dashboard provides a summary of monthly and yearly payments, while showing which policies are optimal and which need some attention

The first advisory component of Clark sees an independent evaluation of existing contracts. It works by automatically checking the insurance contracts in order to identify potential savings or “insurance gaps.” This robo-advisory capability was developed by insurance experts and developers with a rules-based formula that took six weeks to develop.

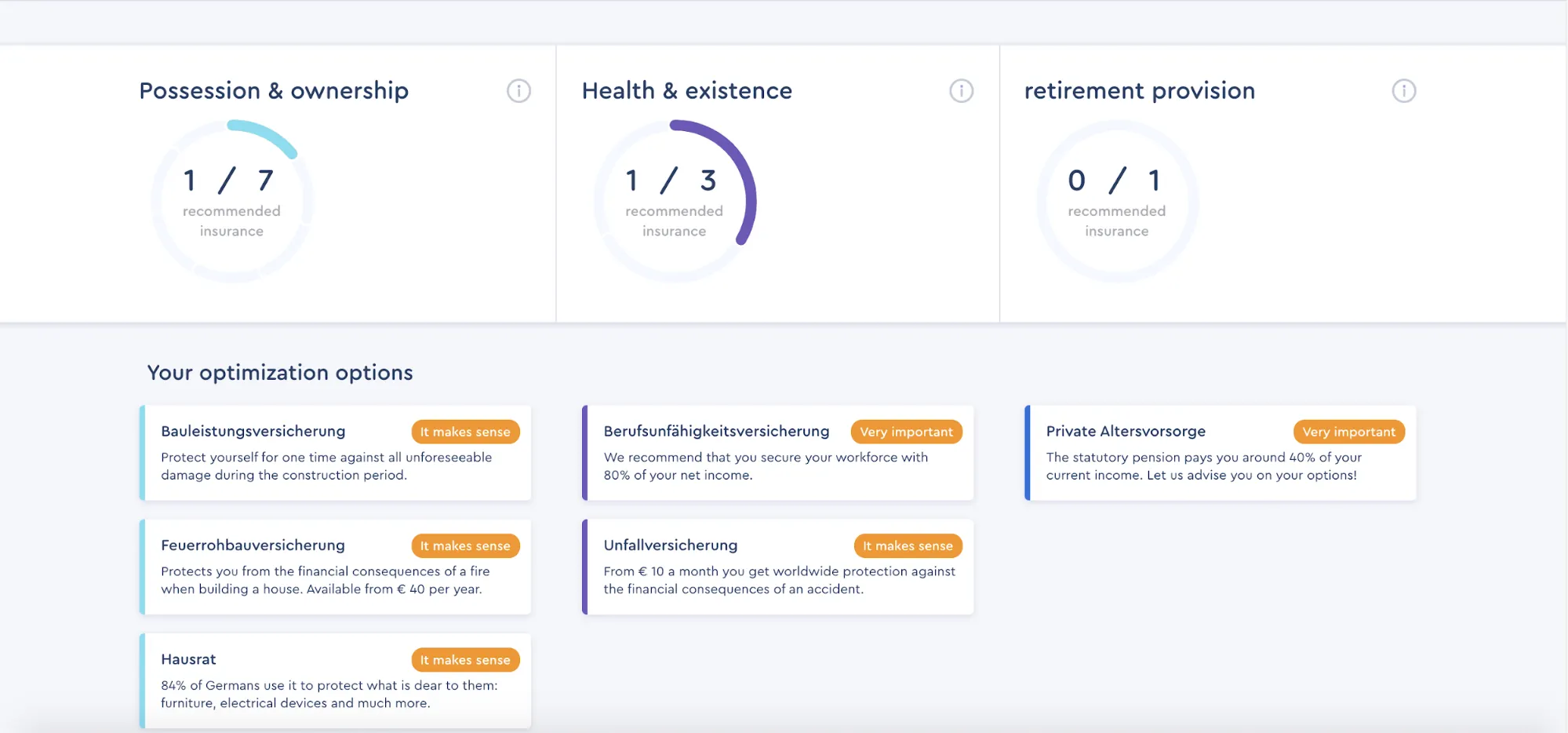

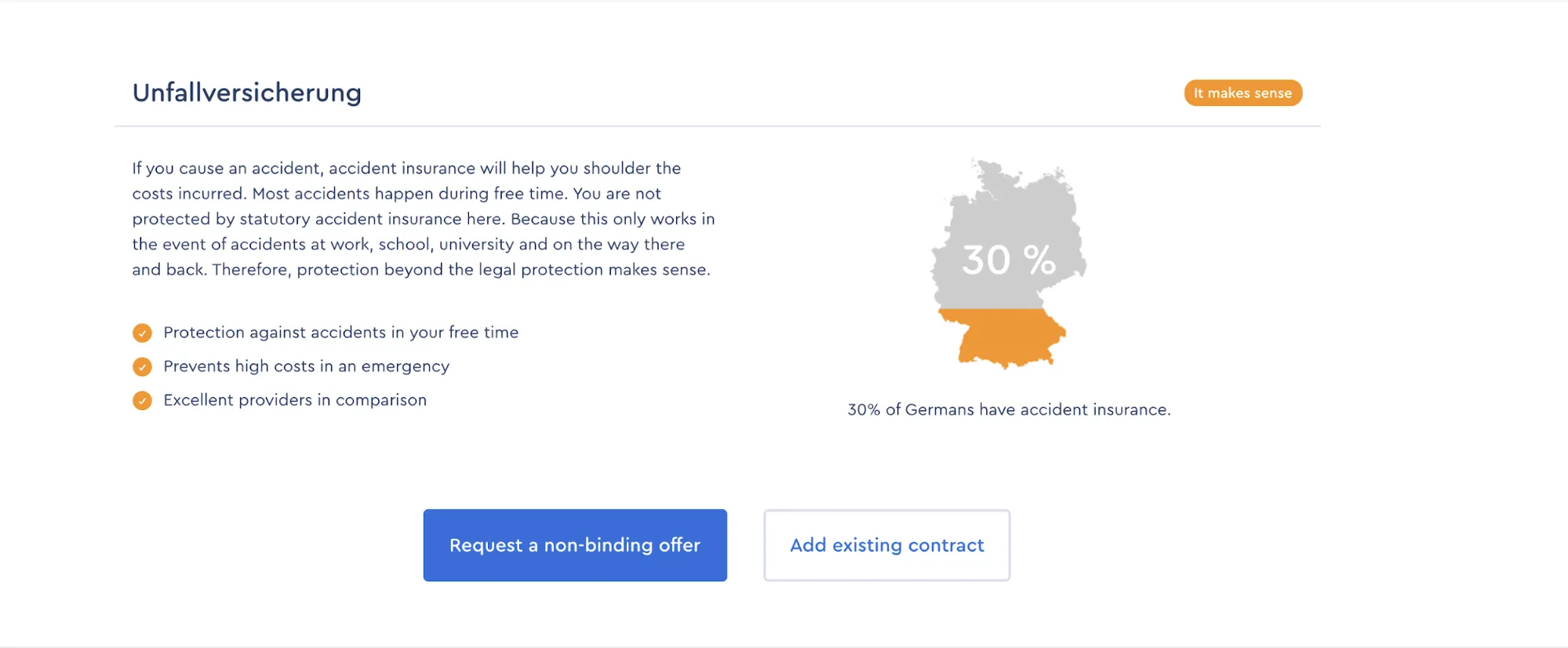

The second part of the advisory component provides customers with quick check-ups on to what extent they are fully covered and this covers a wide spectrum of insurance types. The check-up takes 2 minutes and includes 9 questions, such as the type of home you live in, if you own a car, frequency of travel. Upon completing the check, customers are brought to their dashboard that segments are insured into three categories: possession and ownership insurances, health and accident and retirement. Below each of these are the insurance options for optimising coverage, with further information about what is a priority and what “makes sense.”

Summary of the check-up, which gives the customer an easy to digest overview of policy gaps

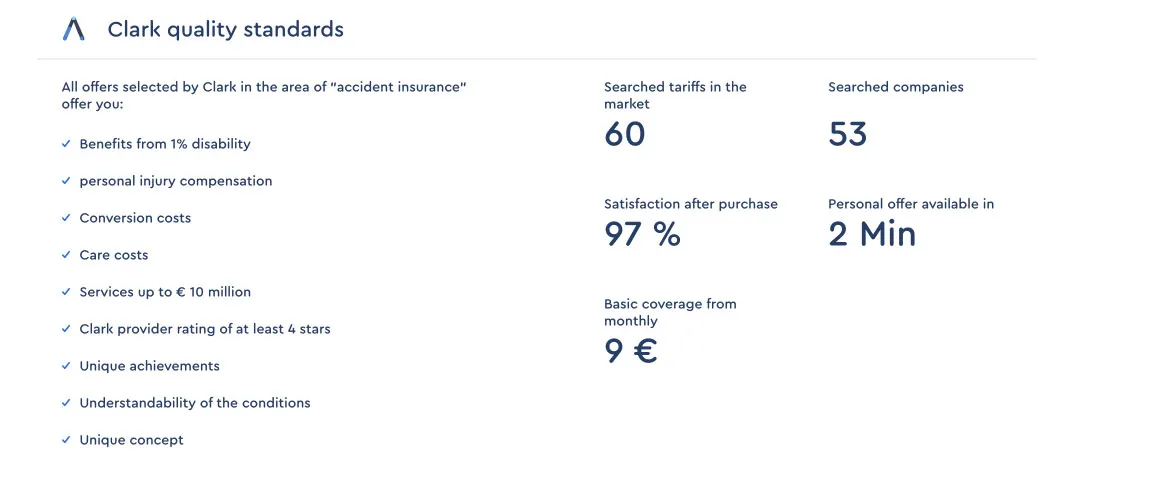

Discovering more information about a specific insurance brings us to the fulfilment component of Clark. Here customers can find out further information about the insurance, and also understand what percent of Germans have the specific insurance. Clark further piques customers interest by providing a very basic case study, and an overview of Clark’s quality standards, including how many companies they have searched, what percentage of customers are satisfied after taking out the insurance, how many tariffs were searched etc.

A summary to further entice customers

Completing the fulfilment journey requires opting for a non-binding offer. Customers answer a few questions, depending on the specific insurance type and then their offer is created, although the offer is not instantly promoted to the user.

In summary, Clark brings a much needed digital, holistic offering to a complex and often fragmented insurance market in Germany. It is not far off from the account aggregators we are seeing in the banking world, utilising existing products held to ensure the customers are in the best financial position.

Following the Fintech path

We have discussed in detail how two insurtechs have changed the customer experience for the better, solving the pain points around management, and relevant products and services. Insurtechs are following a similar path to their fintech counterparts, competing on sleek design, being digital-first, and price. The concept of policy aggregation and advice is similar to bank account aggregation providers, although with perhaps greater potential, as the majority of insurance policies expire and the need for shopping around is greater than say a current account.

Looking to what’s ahead, we can expect a similar path between insurtechs and fintechs in their quest for leveraging smart data to win customers. In the final article of this series, we will explore how leading InsureTechs are leveraging smart data for innovation.

Photography — Arturo Castaneyra via Unsplash